Do you know the impacts of the Fundamental Review of the Trading Book (FRTB) on Banks ?

The 2009 “Revisions to the Basel II market risk framework”(Basel 2.5) was the first attempt by the Basel Committee on Banking Supervision (BCBS) to address the trading book issues revealed by the global financial crisis. The implementation of Basel 2.5 resulted in a significant increase in the regulatory capital requirement for market risk in the trading book. However, this change introduced some inconsistencies in trading book risk measurement, and a substantial increase in regulatory capital charges both in absolute terms and relative to economic capital calculations. Also, Basel 2.5 did not fundamentally address other significant issues, such as the definition of the trading book, the weaknesses of the VaR risk metric, the need for a more comprehensive and coherent risk measure, and the Standardized Approach not being a credible fallback for internal models. The BCBS responded to those shortcomings by launching the FRTB.

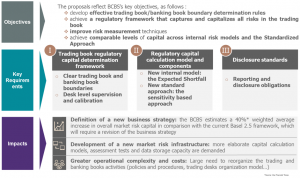

Since May 2012, the BCBS issued 3 consultative documents referred to as the Fundamental Review of the Trading Book (FRTB) and conducted 4 Quantitative Impact Studies (QIS). This led to the publication on January 2016 of the final documentation: “Standards: Minimum capital requirements for Market Risk” which replaces the existing minimum capital requirements for market risks in the global regulatory framework. The changes required aim at ensuring that the standardized and internal model approaches to market risk deliver credible capital outcomes and promote consistent implementation of the standards across jurisdictions. The new requirements include a clear definition of the trading book, new market risk capital calculation models, and the supervision of internal risk models.

From the design of the basic model used to measure risk, to the process for deciding what sits in the banking and trading books. While Basel 2.5 was implemented in the immediate aftermath of the financial crisis as a stop-gap measure to lift trading book capital requirements, the FRTB primarily aims at consolidating existing measures and reducing variability in capital levels across bank.

FRTB Objectives, Key requirements and Impacts

FRTB Open Items

Although the BCBS final rules were published on January 2016, the following points will evolve further prior to the effective date.

Standardized approach floors

Standardized approach floors to the internal models approach charges will undergo further calibrations, to allow the SA to provide a credible fallback when a bank’s internal market risk model is deemed inadequate.

Profit and Loss attribution

P&L attribution test (performed to determine if a desk can be eligible to the internal model) threshold might evolve depending on the findings of the ongoing monitoring.

Credit valuation adjustment (CVA)

The Committee has issued a proposal on the application of the market risk framework to credit valuation adjustments. The CVA standard will be completed and included in the FRTB framework on a stand-alone basis.

- Definition: CVA risk is the risk of loss caused by changes in the credit spread of a counterparty due to changes in its credit quality

- Scope of application: Under the CRR (Capital Requirements Regulation), credit institutions and investment firms are required to hold additional own funds due to CVA risk arising from OTC derivatives (other than credit derivatives used for credit risk mitigation (CRM) purposes) and, if CVA risk exposures are material, securities financing transactions.

- CVA capital charge under Basel III, 2 calculation approaches : Advanced method and Standardized method

- Reviewed CVA capital charge, 3 calculation approaches :

- FRTB CVA : IMA-CVA or SA-CVA

- Basic CVA (when the institutions is not eligible to FRTB CVA)

- Features of the new proposed framework:

- Covers exposure risk and associated hedges

- Explores a move closer to accounting CVA (calculation based on FO exposure models)

- Is closely aligned with new requirements for market risk in the trading book (calibration to ES)

Synthesis – FRTB Impact Matrix

Sources : BCBS publications

- Consultative document Review of the Credit Valuation Adjustment Risk Framework BCBS (July 2015)

- Fundamental review of the trading book – interim impact analysis – BCBS (November 2015)

- Revisions to the Standardized Approach for credit risk – Second consultative document – BCBS (December 2015)

- Standards – Minimum capital requirements for Market Risk – BCBS (January 2016)

- Pillar 3 disclosure requirements – Consolidated and enhanced Framework – BCBS (March 2016)